Stefán Ólafsson writes:

Those who have the highest incomes usually have a large part of their earnings in the form of capital income, which is taxed much lower than the wages of the general workforce. The highest income percentile, for example, has the majority of its total income in the form of capital income, whereas for the rest of the general workforce, capital income is only a fraction of total income.

Fjármagnstekjur eru þannig langmestar hjá þeim tekjuhæstu.[i] Skattfríðindin sem fylgja lægri álagningu á fjármagnstekjur eru gríðarleg og renna einkum til þeirra sem þurfa alls ekki á þeim að halda

In this article I assess the extent of these tax breaks for the highest earners and compare the amount with the state's expenditures on child benefits and housing support for low‑income households. The support for those highest earners is twice as large as the support for those low‑income.

But first let's examine the extent of the tax benefits that are hidden in the unusually low taxation of capital gains.

Scope of tax benefits on capital income

Capital gains are income from assets. They consist of dividends from stocks, capital gains, interest income and rental income. Capital gains are now taxed with a 22% surcharge above the personal allowance. The tax on employment income and pensions is in three brackets: 32%, 38% and 46% on income above the personal allowance.

Wage incomes of 472 thousand per month have a 32% surcharge in income tax and surtax, or about 10 percentage points higher than the surcharge on capital income. Those who have 472 thousand in wages per month are close to the poverty line.

Public revenue from capital gains tax in 2023 was about 73 billion. If the surcharge on capital gains this year had been the same as the middle bracket of income tax that the public pays (i.e., 38%), then public revenue from capital gains tax would have been about 52.4 billion higher that year, or about 125 billion instead of 73 billion. If the surcharge had been at the top bracket (about 46%) then public revenue would have been about 79 billion higher. A lot can be done for 52 billion and even more, of course, for 79 billion each year.

Those who have the highest capital income (the wealthiest people) usually also have high labor income or pension income, and therefore their capital income would fall into the top tax bracket (46%) if it were taxed like the general public's labor income. It could therefore be fully justified to use the higher figure as a measure of the tax advantage of capital income.

But we take the more modest route and use the lower figure as a general measure of tax benefits from capital gains – i.e., 52.4 billion per year. Then we examine what value these benefits have in comparison with some important public expenditure items in the same year. That puts the benefits in the context of society.

If the capital gains of the highest earners were taxed like the wages of the general workforce, at the median income tax rate (38%), the state would have about 52 billion extra per year to devote to field operations and welfare matters for the benefit of the public.

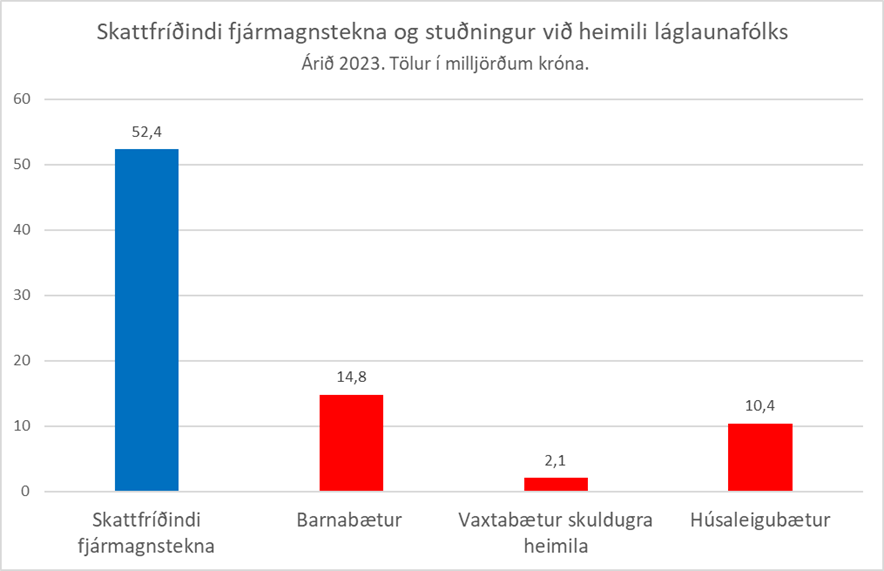

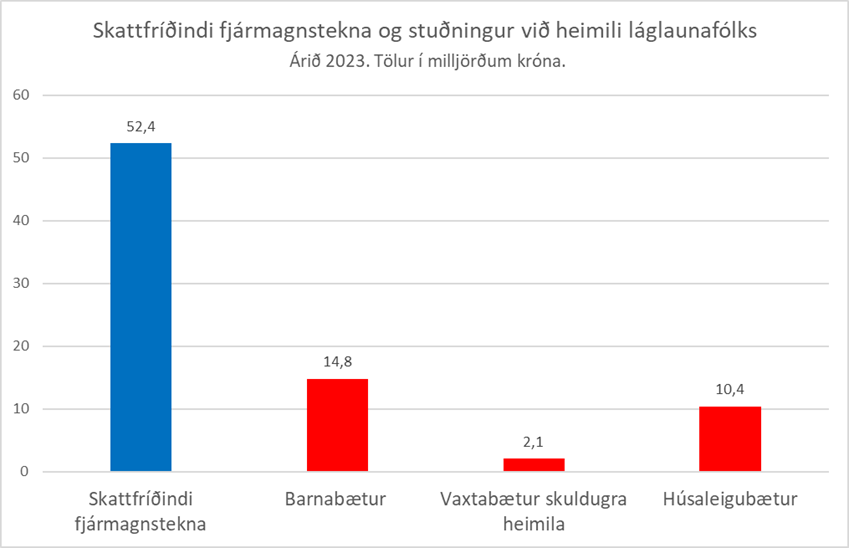

Much greater support for the higher earners than for the lower earners

In the figure we compare the scope of tax benefits on capital income and the state's expenditure on the main aspects of support for households of wage earners in lower and middle income groups, i.e., support for the establishment of families and households at the time when people's burdens are greatest in their career.

These are transfers to children in the form of child benefits, interest subsidies to indebted households, and finally expenditures for rent subsidies to low-income people who live with high rent.

As the figure clearly shows, the state's cost from tax breaks due to capital gains is much higher than the cost of paying child benefits (52.4 billion versus 14.8). The cost of housing support (interest and rent subsidies) is almost negligible compared to the cost of benefits from capital gains.

The total cost to the state of all these three support measures for low‑income households is about 27 billion. The state's support for the highest‑earning and wealthiest households, with lower taxation on capital income, is thus almost double the support for low‑income households. Before the tax on capital income was significantly reduced (1997), expenditures for assistance to households of working people were nearly three times higher than they are now. Prior to 1997, capital income was taxed mostly like wages.

Alongside the increased tax breaks for the higher‑earning and wealthier, support for households was lower and between income groups thus greatly distorted. The welfare system of the rich flourished while the welfare system of lower‑income earners was squeezed.

The policy of ASÍ is that capital income should be taxed again like wage income. With the above correction of the capital income tax, it would bring about five times more revenue for the state than is obtained by raising hunting fees.

[i] About þetta is ítarlega discussed í in my book and Arnaldar Sölva Kristjánssonar, Ójöfnuður á Íslandi, which was published in 2017. More than two thirds of all capital income are equally shared by the highest income third of earners.

Stefán Ólafsson is professor emeritus at HÍ and works as an expert at Efling trade union.

The article first appears in Heimildin on August 22, 2025.