The board Efling union has sent its proposals to the government regarding the introduction of a rent brake. The proposals have been

send to Prime Minister Kristrún Frostadóttir, Minister of Social Affairs and Housing Ragnar Þór Ingólfsson, and to members of the Welfare Committee of the Althingi.

The introduction of a rent brake in the Icelandic rental market could help reduce inflation, inflation expectations and interest rates quickly. Rent levels in Iceland have risen far more than in neighbouring countries, making rent a distinct driver of inflation in Iceland.

Efling’s proposals include, among other things, a ban on monthly rent increases, annual increases linked to the Consumer Price Index excluding housing costs, clearer limits on the setting of market rents, and stronger oversight.

Efling points out that similar measures have proven successful abroad and refers specifically to Denmark, where a temporary cap on rent increases has contributed to a faster reduction in inflation than otherwise.

In Efling’s view, implementing a rent brake would be both a fast-acting anti-inflation measure and an important improvement in living standards for tenants, especially young and lower-income people. The union calls on the government to take immediate action.

Rent brake reduces inflation

Proposals from the Executive Board of Efling Union to the Government

1. The Icelandic rental market is abnormal

The Icelandic rental market has fewer restrictions on rent increases than in almost all neighboring countries. This has led to residential rents rising much more in Iceland than in most other parts of Europe. For example, rents have risen three times more in Iceland than in the other Nordic countries on average over the past decade.

Rents in Iceland have not only increased monthly, but the annual increase in rents has been three times greater than the increase in the Consumer Price Index (CPI). Thus, rents have been a particular driver of inflation in the country. This applies to both residential and commercial rents.

It is therefore in the interest of society and workers in particular to bring the rental market structure here into line with that of most of our neighboring countries. This could be a major and immediate step in the fight to reduce inflation, inflation expectations, and the interest rate in the country.

2. Efling’s proposals

Efling recommends that the government address these issues firmly and promptly. Efling proposals, which are based on the experience of OECD countries, cover five important aspects, all of which must be met in order to achieve success. The proposals are as follows:

1. Ban monthly rent increases. Instead, annual increases will be introduced, based on the start date of the lease agreement (as is common practice in many places).

2. rental properties

residential and commercial

3. Annual increases in rent in the general market will not exceed the increase

in the consumer price index excluding housing. This will initially be in effect for the duration of the collective bargaining agreement (i.e. until 2028). This would

reduce the interaction between housing market inflation and general price levels.

4. Restrictions will be placed on

determining rent at the start or renewal of a lease, so that the rent is not higher than for comparable housing on the market at that time (this is similar to what is common in Norway, Denmark, Sweden, Germany and elsewhere).

Statistics Iceland will regularly publish the amount of average rent by type of housing and location, which will be

a guiding criterion when drawing up leases.

5. Monitoring by HMS of market rent developments should be strengthened, and tenant consumer protections should also be reinforced.

The Minister of Social Affairs and Housing has announced plans to ban monthly rent increases, which is a good first step. But all the other steps also need to be taken to achieve sufficient success in the fight against inflation and lowering interest rates. This is what is needed to bring the Icelandic rental market into line with that of many neighboring countries. This is also a major wage issue for workers, especially younger and lower-income workers, who are generally more stuck in rented housing than other social groups, while nearly 30% of the country's population now lives in rented housing.

3. The Danish example

When inflation rose from 1.9% to around 8% in Denmark, following Russia's invasion of Ukraine in 2022, Metta Fredriksen's government temporarily set a ceiling on annual rent increases at 4%, or about half of the inflation rate at the time. This was in effect for 2 years. Inflation fell to around 3% the following year. A rent brake can thus be a very quick and powerful brake on general price increases.

4. General arguments and data

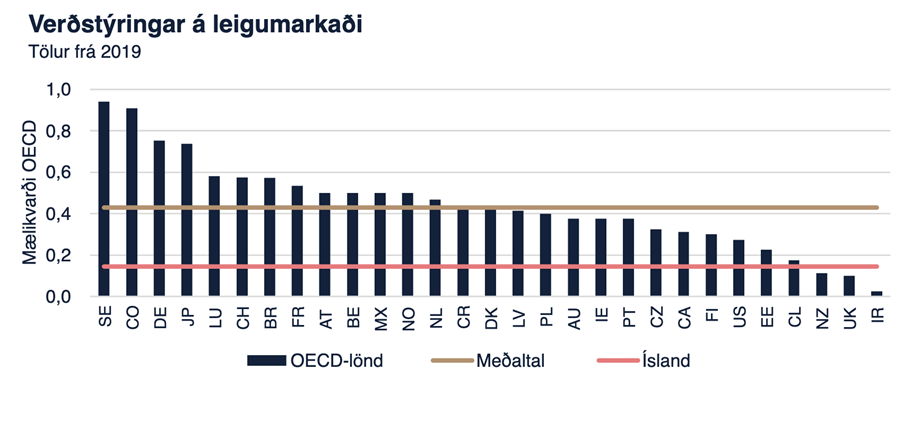

The Icelandic rental market is less restrictive of rent increases than is common in neighboring countries. Only 3 of the 29 OECD member countries have fewer restrictions on rent increases than Iceland (see Figure 1 in the Appendix). Even the United States imposes more restrictions on rent increases than Iceland. Iceland has a de facto record for government indifference to the rental market.

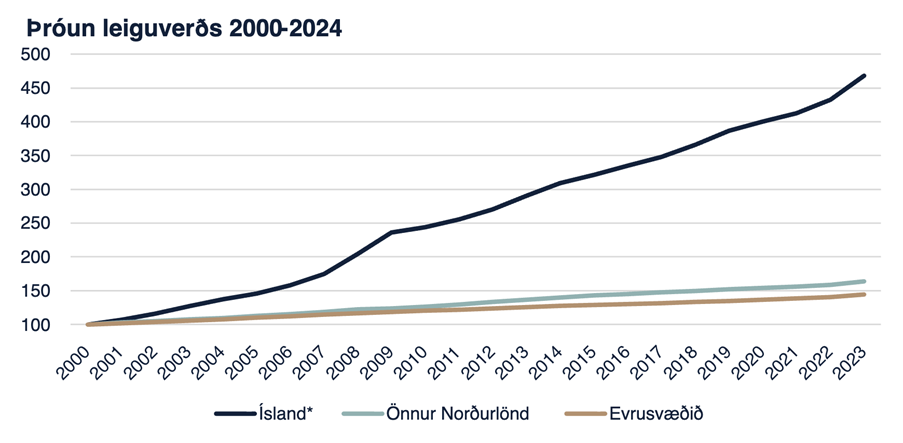

It has therefore been unusually easy for Icelandic landlords to raise rents above those in neighboring countries, for both apartments and commercial properties. As might be expected, this has resulted in much larger rent increases in Iceland (see Figure 2 in the Appendix).

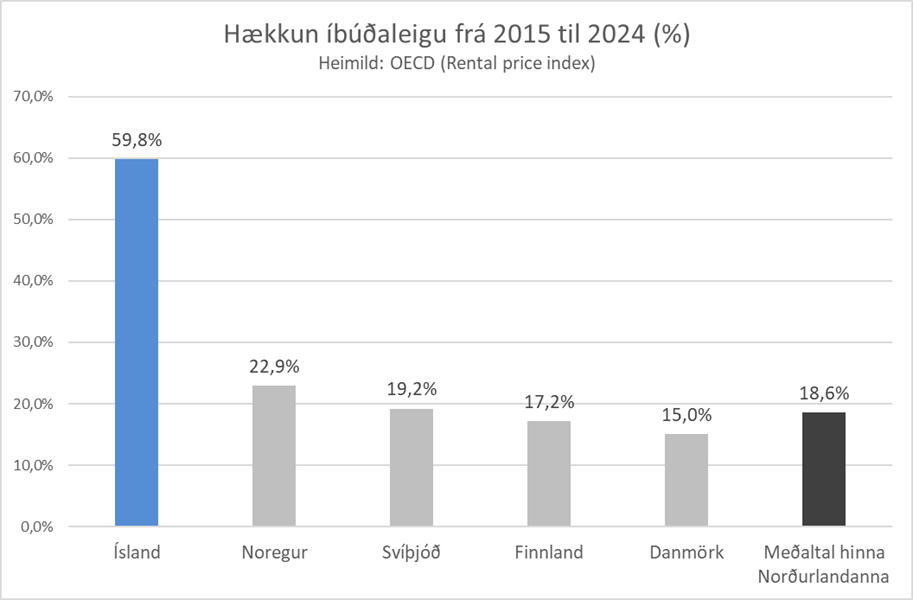

For example, residential rents have risen three times more in Iceland than in the other Nordic countries between 2015 and 2024 (see Figure 3 in the Appendix). Rents here have risen far in excess of general increases in consumer prices (the CPI), and therefore rents are generally an independent driver of inflation.

Monthly rent increases mean that rent is the leading inflationary pressure (negotiated wages and public spending generally do not increase monthly, but annually). The rent increase then enters the inflation measurement – and then becomes a reason for further rent increases, in an inflationary interaction of increases. Frequent increases in the leasing of commercial premises to companies are directly reflected in the price level.

This is a completely unacceptable arrangement, which plays a major role in persistent inflation in this country and high interest rates.

The main way for the labor movement to protect workers against excessive increases in rent and housing prices, as well as increases in the prices of necessities, is to try to keep wages in line with these cost increases. If rent and housing prices rise far beyond the purchasing power of workers, this leads to larger wage increases than would otherwise be the case in the future.

A broad coalition of trade unions attempted in the 2024 collective bargaining agreements to reach a national agreement on reducing inflation and interest rates, with a moderate increase in wages for four years, in practice with annual increases smaller than the inflation rate at the beginning of the agreement period.

Now it is the turn of landlords to show similar restraint to reduce inflationary pressure from the rental market. Landlords profit in two ways: through excessive rent increases and through unusually high housing prices, which increases the landlords' equity in the rental apartments.

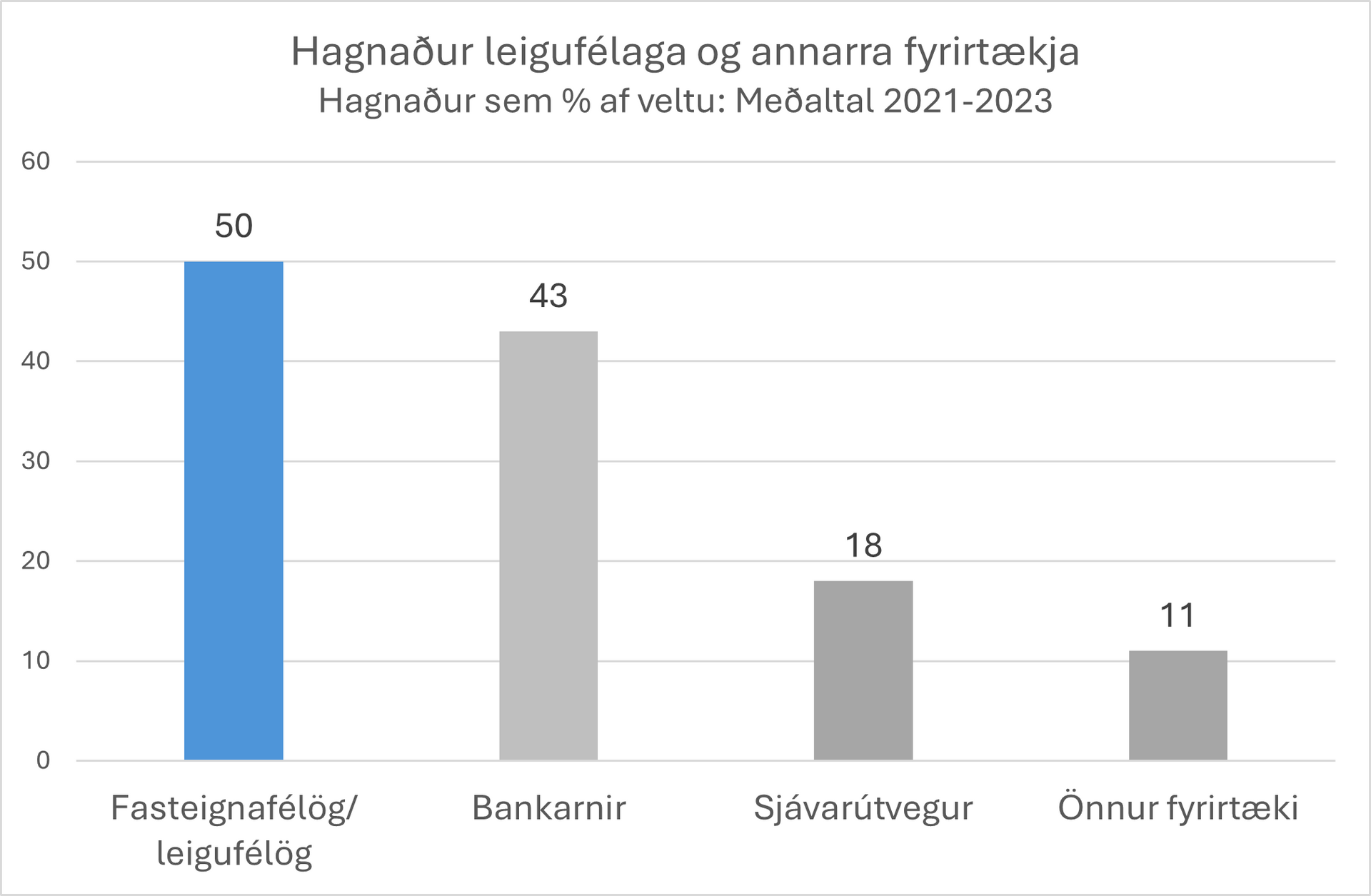

This is a double profit machine. Landlords have thus made enormous profits from their operations in recent years. Private market landlords have even had a higher percentage of profit on turnover than banks (see Figure 5 in the Appendix).

The same restraint would also need to apply to the prices of housing and other essential goods, as well as to public fees.

A national agreement to quickly achieve the Central Bank's target of 2.5% inflation should then mean that landlords, housing agents, public entities and sellers of goods and services limit their annual increases to 2.5% throughout the agreement period until 2028. Due to the high risk of a further increase in import prices in the near future, however, increases could be limited to the price index excluding housing during the period. This should ensure acceptable operating results for landlords, i.e. in line with other activities in the business economy.

What could a rent brake achieve in Iceland now?

After record increases in both rent and housing prices over the past 10-15 years, housing prices in Iceland have become far too high, whether for purchase or rental. Young people are having to take on enormous amounts of debt to acquire an apartment, and renters are finding it increasingly difficult to save up for a down payment on an apartment. The number of people who can afford the necessary debt repayments is steadily decreasing, especially after banks have recently tightened mortgage lending standards even further.

Direct reductions in these housing costs, which depend, among other things, on the interaction of supply and demand, would need to occur. But that takes longer.

Now, however, it is possible to take control and rein in the unbridled rental market to begin with. This would ensure that the situation does not continue to deteriorate, but would improve through gradual adjustment. Inflationary pressures would decrease. This would include wage improvements for tenants in general and especially young people with lower and middle incomes.

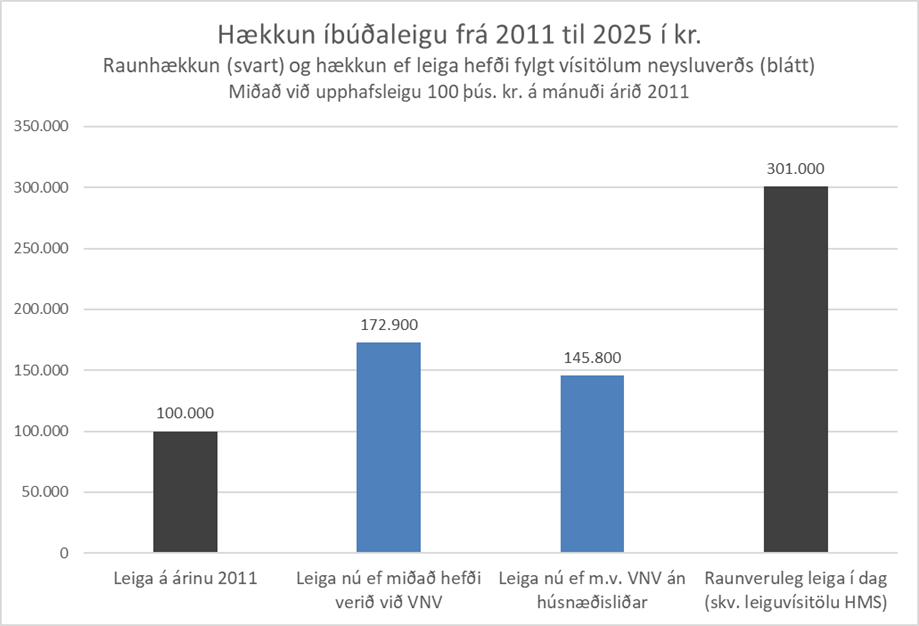

Figure 4 in the appendix shows what the impact of the measures now proposed by Efling would have been if they had been applied to rental prices from 2011 to 2025.

It states that housing that was rented for 100 thousand ISK per month in 2011 is today rented for about 300 thousand ISK (according to an extrapolation of the HMS rental index). The rent has tripled.

If rent had only increased by annual linkage to the Statistics Iceland consumer price index (CPI), the rent for the same housing today would be almost 173 thousand krónur per month. If linkage had been to the consumer price index without the housing component (which would be most reasonable), the rent for the same housing would be around 146 thousand krónur today, not around 300 thousand krónur. The rent would be half as much.

Such restrictions on rent increases would stop the independent upward impact of rent on inflation, rapidly reduce inflation expectations, and strengthen economic stability.

This would also be a major issue for tenants, who now make up close to 30% of the country's population and are often the lowest-income earners.

The introduction of a moderate rent brake, as Efling suggests, does not cost the state any additional expenses, but can improve the performance of the public sector, which is often in the position of a tenant. A rent brake can be implemented quickly, as the Danish experience shows. Efling therefore calls on the government to implement the rent brake quickly and effectively.

______________________________________________________________________________

Appendix:

Data on rental market regulation and rent increases