Board Efling of the union has decided to fund Matthildi, an organization for harm reduction, with 1.7 million kronur. The Matthildi organization was founded in 2022 and focuses on harm‑reduction services at the early stages of substance abuse. The aim of harm reduction is to help people stay alive, protect their health, both physical and mental, and to empower them in all small steps towards positive change. Matthildi runs the harm‑reduction service Reyk. The service is free of charge for everyone and places a special emphasis on reaching people at the early stages of substance abuse, with the aim of preventing a more serious development of the problem and untimely deaths. In the period from 4 February 2025 to 31 January 2026, Reyk has provided service to 235 individuals on 1,100 occasions. Of these, 25 percent of the clients are employed, and some of them are members of Efling. These individuals struggle with substance abuse as well as poverty and difficult social circumstances. A steady increase in opioid problems has occurred over the past nearly fifteen years. In addition, problems related to cocaine use, crack and methamphetamine smoking have risen steadily over the last decade. It is very important to provide the group facing this problem with harm‑reduction services and support for recovery. The Reyk service is for many the first point of contact for assistance and provides clients with extensive support, follow‑up and connection to social and health services. Matthildi has assisted many in substance‑use treatment, opioid medication treatment and obtaining appropriate social services. In doing so, the organization has helped individuals recover and be able to keep housing, mental health and continue working.

The board of Efling union approved at its meeting on May 13 a support declaration for strike actions of Norwegian members in the cleaning sector within the sister union Norsk Arbeidsmandsforbund. In the declaration, colleagues in Norway sendr are sent struggle and solidarity greetings. The declaration follows below. The board Efling sends struggle greetings and expresses full support for the strike actions of staff in the Norwegian cleaning sector under the leadership of our sister union NAF. The members of Efling recognize the courage and the great work required to organize an effective strike. The board is also well aware of the necessity to improve the terms and conditions of workers in the cleaning sector worldwide, including in Iceland and Norway. Efling believes in the power of the union and wishes our collaborators in Norway the best possible success in their struggle. Norwegian version Efling expresses support for Norwegian colleagues in strike. The board of the Efling union adopted at its meeting on May 13 a support statement for the strike actions among Norwegian colleagues in the cleaning industry within the sister union Norsk Arbeidsmandsforbund. The declaration includes messages of struggle and solidarity to the colleagues in Norway. The declaration follows below. The board of Efling sends a greeting of full solidarity with the striking workers in the Norwegian cleaning sector, led by our sister union NAF. The members of Efling know what courage and hard work are required to organize a successful strike. The board is also aware of the need to improve the terms and conditions for workers in the cleaning industry globally, including in Iceland and Norway. Efling believes in the power of collective action and wishes our colleagues in Norway the greatest possible victory in their struggle.

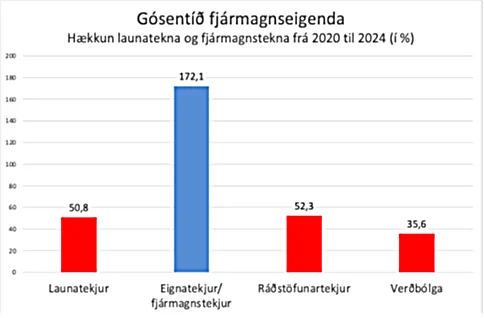

Stefán Ólafsson writes: The Central Bank is cooling the economy, hoping to bring down inflation. It does this by keeping interest rates high, which bites at indebted households and businesses. However, it does not work on foreign price increases, nor on inflation due to rising housing costs, nor on demand expansion of indebted and high‑income individuals and companies, nor on expansion due to private consumption of a large number of tourists. These measures of the Central Bank have ultimately shown to deliver only limited results and are increasingly extremely unfair in the distribution of burdens. But the Central Bank's method certainly cools the economy, it almost reduces economic growth and increases unemployment. That is the cost of applying the high‑interest policy. Recently the analysis department of Landsbankinn published its economic forecast for the years 2026 to 2028, which assumes growth of only 1.6 to 1.8% over the next three years. That is less than the projected population growth in the country, according to the Statistics Iceland forecast. Growth per capita will therefore be negative. In reality, this means that the economy has entered a stagnation that is expected to continue at least until 2028. This can be seen in the picture below, which shows growth per capita.